In 2018, the Life Sciences (LS) industry continued to struggle with achieving growth and accelerating time-to-market amid the challenges of rising costs, pricing regulations, and policy changes. Digital transformation had been identified by many enterprises as a strategic imperative to combat these challenges. However, many of the life sciences firms that tried to implement digital strategies internally failed, and the industry as a whole still yearns for digital maturity. Enterprises are now looking for thought leaders and execution champions that can help them on their digitization journey.

In 2019, we expect an uptake in digital deals as LS firms continue their journey of digital transformation. Service providers have been making significant efforts around ramping up their digital capabilities and proprietary solutions portfolio. What remains to be seen is whether these investments can now translate into positive business outcomes for enterprises.

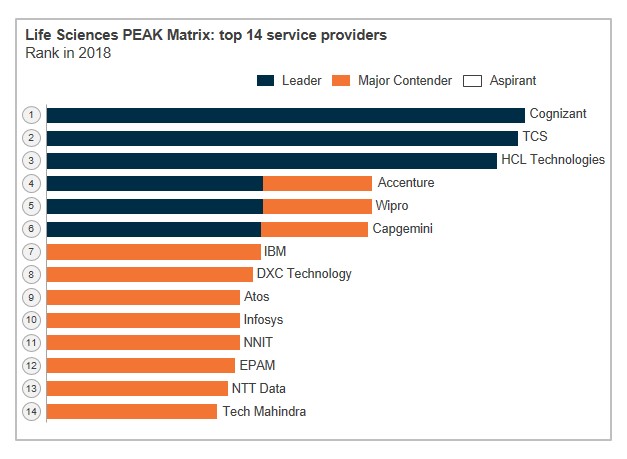

This report examines the global 2018 Life Sciences BPS and ITS service provider landscape and covers the outlook for 2019. It focuses on service provider positioning in 2018’s two Life Sciences PEAK Matrix evaluations; Life Sciences Digital in North America and Life Sciences Digital in Europe. It also identifies key market trends observed in 2018, as well as technological themes expected to garner greater interest in 2019.

The report is structured across two key sections:

Demand overview

Life sciences trends observed in 2018

Key developments observed at life sciences enterprises

Life sciences IT services market analysis

Outlook for 2019

Analysis of major deals up for renewal

Service provider landscape

Ranking of service providers based on their performance in 2018’s life sciences PEAK Matrix evaluations

Introduction

The healthcare landscape has been subject to significant turbulence on account of a gamut of factors including escalating costs, widespread regulatory amendments, changing business models, and evolution of the patient-centric paradigm…