|

|

Property & Casualty (P&C) Insurance BPO: Addressing Growth Through Digital Empowerment

29 Jun 2018

by

Somya Bhadola

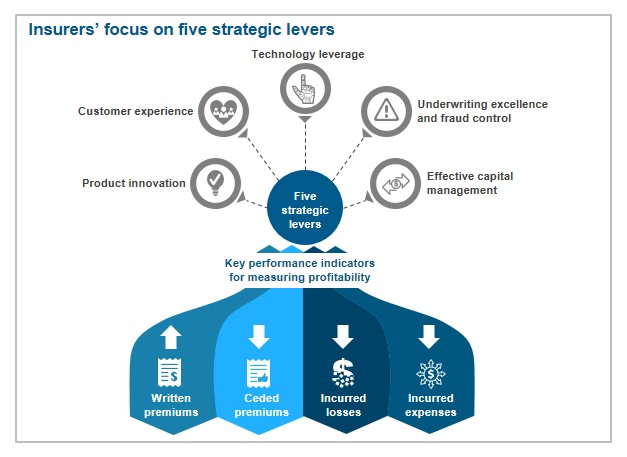

The P&C insurance industry is heavily dynamic at present, with multiple macro- and micro-level factors impacting the insurers’ operations. In such a scenario, all P&C insurers are facing a significant question – how to be profitable while growing? While there can be no single answer to such a strategic question, a combination of five strategic levers has been identified, which would assist insurers in riding the market dynamics in a planned manner.

The market dynamics referred to above have trickled down to the P&C insurance BPO industry as well. Consequently, a few BPO service providers are stepping-up to assist insurers in mitigating their present challenges. Service providers are leveraging domain expertise for consulting and design thinking services and technologies such as automation for increasing operational efficiencies and analytics for greater value-addition. These are over and above the usual cost savings that are associated with an outsourced delivery model.

Thus, the P&C insurance BPO market has been consistently growing at ~13% from 2015-2017, and the market growth is only expected to accelerate in the future. Leveraging technology and domain expertise, in addition to scope expansion of services beyond the transactional ones, would be key enablers for service providers to expand the P&C insurance BPO market. Geographically, North America continues to drive BPO adoption, while the European market is plagued by geopolitical and regulatory pressures, such as Brexit and GDPR, that have impacted deal signings in Europe.

Scope and Methodology

- Proprietary database of 430+ P&C insurance BPO contracts (updated annually)

- Coverage of 20+ P&C insurance BPO service providers including Accenture, Capgemini, Capita, Cognizant, Conduent, DXC Technology, EXL, Genpact, HCL, Infosys, Intelenet, NIIT Technologies, Shearwater Health, Sutherland, Syntel, TCS, Tech Mahindra, and WNS

Content

This report provides comprehensive coverage of the global P&C insurance BPO market, including adoption trends across geographies, buyer size, factors impacting the market, key solution characteristics, emerging trends, and service provider landscape. It will assist key stakeholders (P&C insurers, service providers, TPAs, and technology providers) to understand the changing dynamics of the P&C insurance BPO market and identifying the upcoming trends. Some of the findings in this report are:

- With rising dynamism in the P&C insurance industry, insurers are facing multiple challenges. The impact of these dynamics is that insurers are finding it difficult to achieve profitable growth

- BPO service providers have started to realize the insurers’ needs. Consequently, they have augmented their offerings and have started to layer BPO services with technology

- The P&C insurance BPO market has been growing at ~13% and is likely to grow at a further accelerated rate of 13-15% in the coming years

- North America continues to offer the highest potential among other geographies for P&C insurance BPO service providers, in terms of new contracts signings

- Claims processing in P&C insurance has emerged as a potential target area for BPO service providers. This is driven by insurers’ strategic requirements and providers’ ability to meet them

- As buyers look at expanding their partnerships from just outsourcing of administration to value-addition across operations, technology capabilities and domain expertise of service providers will play a significant role

Membership(s)

Insurance – Business Process Outsourcing (BPO)

Page Count: 60

|

|