|

|

Healthcare Payer BPO Market – Deal Trends Report 2018

29 Jun 2018

by

Manu Aggarwal, Ankur Verma, Naman Sharma

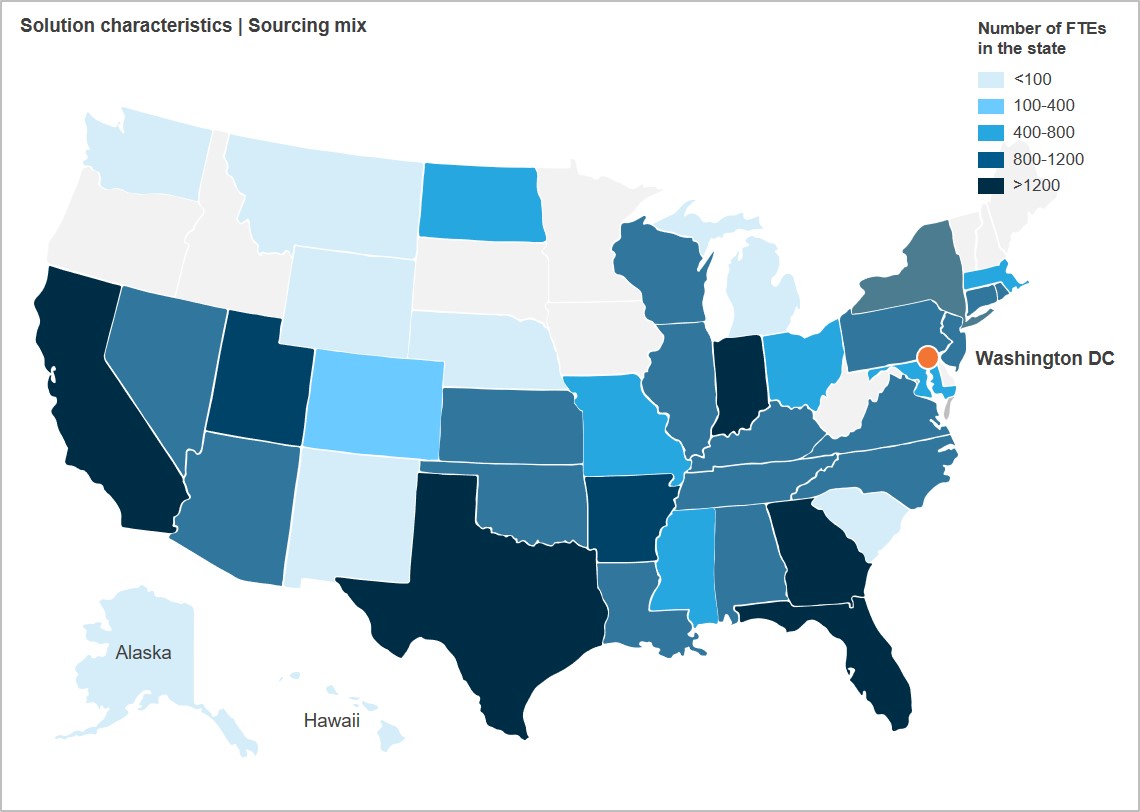

After a year of stalled investments owing to market uncertainty, healthcare payers restarted investments in areas such as value-based care adoption, care management, utilization & disease management, population health, and consumer experience. On the technology front, automation, analytics, and BPaaS continue to be areas of interest for the healthcare community. In fact, inclusion of analytics in total contracts is reaching a whopping ~50%. Outsourcing – both traditional and technology-focused – is expected to continue growing at a healthy double-digit rate in near future.

In this research study, we look at the healthcare payer BPO market from the point of view of adoption trends as well as prevalent solution characteristics.

Some of the findings in this report are:

- The healthcare payer BPO market witnessed a spike after a year of slow growth, with the market reaching ~US$11 billion in 2017

- KPIs for outsourcing are moving away from cost towards new-generation metrics such as innovation, domain expertise, and digital knowhow

- Outcome-based contracts – based on factors such as NPS scores and claims settled – are coming to mainstream; however, transactional pricing has maximum penetration

- Manila is the biggest and one of the fastest growing offshore locations for healthcare payer outsourcing services

- Several trends are shaping how healthcare stakeholders act and have an indirect impact on the service providers too

- In addition, service providers themselves are under pressure from other market participants and are trying to reinvent existing business models

- Accenture, Cognizant, Conduent, and DXC Technology continue to lead the market, both in terms of revenue and number of clients

- Claims management, followed by member engagement, continues to be the largest and most competitive space

Membership(s)

Healthcare & Life Sciences Business Process Outsourcing

Page Count: 35

|

|