Navigating the Platform Odyssey: Software Product Engineering Services PEAK Matrix® Assessment 2024

PEAK Matrix® Report

In the product engineering space, software remains the largest area of expenditure, maintaining its upward trajectory despite a slower pace. This deceleration is primarily due to recessionary headwinds, geopolitical conflicts, talent shortages, and delayed decision-making within enterprises. Amid this macroeconomic turbulence, several themes continue to drive software R&D forward. These include transitioning to platform-based business models, increasing the adoption of AI- and gen AI-augmented secure products, prioritizing sustainability, and enhancing customer and developer experiences.

The shift toward these transformative themes, coupled with the current economic climate, is significantly altering enterprises’ expectations from their providers. Rather than solely seeking providers focused on offering engineering talent, enterprises now aspire to engage with strategic partners capable of delivering savings, speed, and innovation simultaneously.

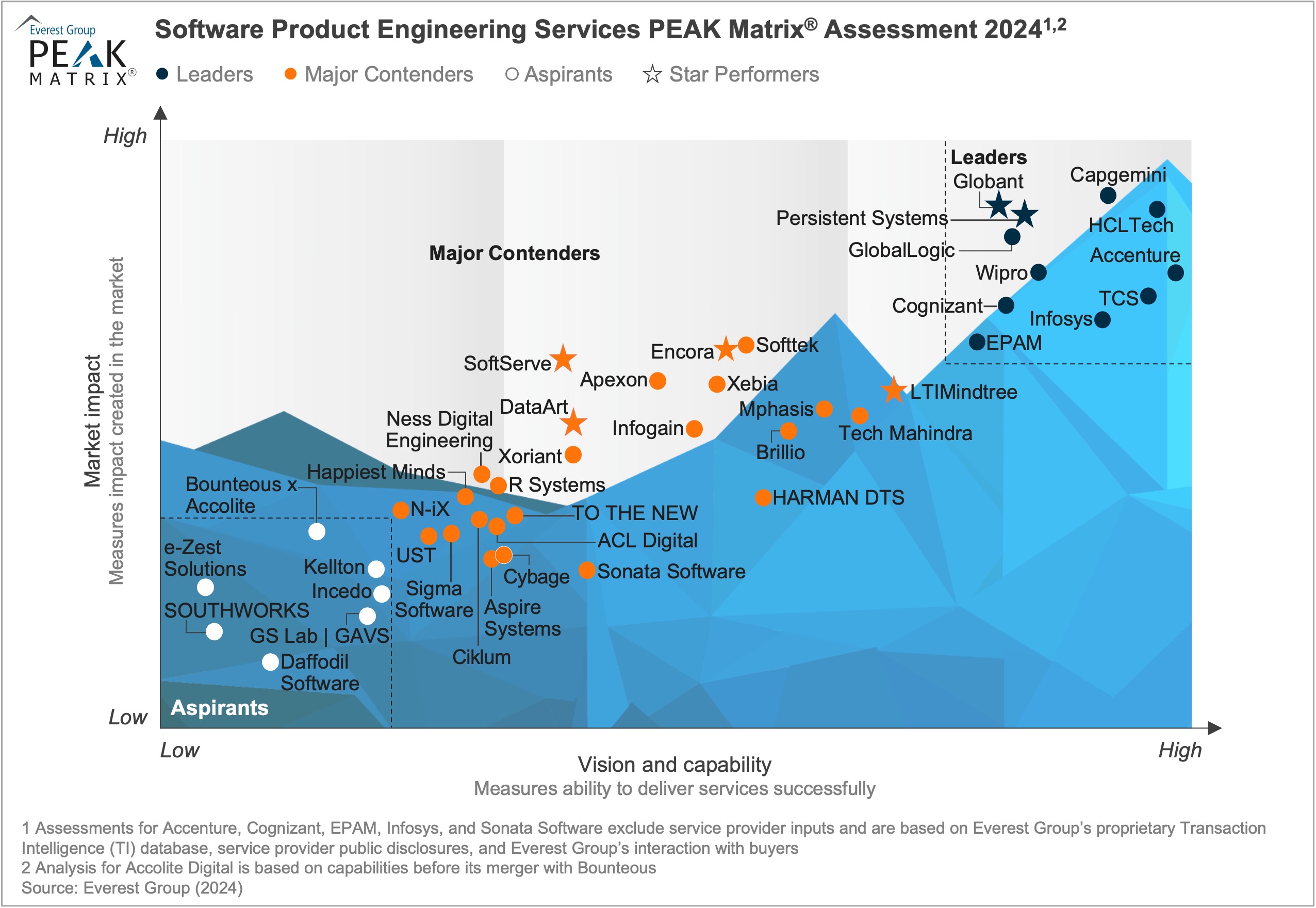

This report, the fifth edition of Everest Group’s Software Product Engineering Services PEAK Matrix® Assessment, evaluates 43 engineering service providers, positioning them on the PEAK Matrix® framework and offering insights into enterprise sourcing considerations.

Scope

- Industry: software product engineering

- Geography: global

- The study is based on RFI responses from providers, interactions with their software product engineering services leadership, client reference checks, and an ongoing analysis of the software product engineering services market

Contents

In this report, we examine:

- Everest Group’s services PEAK Matrix® evaluation of engineering service providers associated with software product engineering services

- The characteristics of Leaders, Major Contenders, and Aspirants

- Providers’ market impact and vision and capabilities

- Providers’ key strengths and limitations